Latest Blogs

Software Development

Ramsha Khan

Jun 30, 2026

SOC 2 vs HIPAA: What Healthcare Technology Companies Need to Know

Read More...

SOC 2 vs HIPAA: What Healthcare Technology Companies Ne...

If you run a healthcare technology company in the US, you’ve probably heard both of these terms thrown around in the same breath: SOC 2 and HIPAA. Maybe a hospital client asked for your HIPAA compliance documents. Maybe a venture-backed buyer asked for your SOC 2 report before signing a contract. Maybe both happened in the same week, and now you’re wondering if you need one, the other, or both.

You’re not alone. This is one of the most common points of confusion for healthcare SaaS founders, CTOs, and compliance leads. SOC 2 and HIPAA both deal with protecting sensitive data, but they come from completely different places, serve different audiences, and carry very different consequences if you get them wrong.

This guide breaks down SOC 2 vs HIPAA compliance. We’ll cover:

We’ll also look at how working with the right HIPAA compliance consulting and SOC 2 compliance automation partner, and a dedicated Governance, Risk, and Compliance service built for exactly this kind of decision, can save you months of confusion and rework.

SOC 2 stands for System and Organization Controls 2. It’s a framework created by the American Institute of Certified Public Accountants (AICPA) that helps service organizations show their customers and partners that they take data security seriously.

Think of SOC 2 as a third-party seal of approval. An independent auditor examines your company’s internal controls, things like access management, data encryption, system monitoring, and incident response, and then issues a report confirming whether those controls are designed properly and, in the case of a SOC 2 Type 2 compliance audit, whether they actually worked as intended over a period of time (usually three to twelve months).

SOC 2 is built around five Trust Services Criteria:

Here’s something important: SOC 2 is not a pass-or-fail certification. There’s no “SOC 2 certified” badge you slap on your website. Instead, you get a detailed report that customers, investors, and partners can review to understand exactly how your security program works and how well it performed.

You’ll see people mention “SOC 2 Type 1” and “SOC 2 Type 2 compliance” like they’re interchangeable, but they’re not.

SOC 2 wasn’t built specifically for healthcare. It applies to any service organization that stores, processes, or transmits customer data, whether that’s a fintech app, a marketing platform, a cloud storage provider, or a healthcare SaaS company. Its purpose is to give customers confidence that a vendor has real, working security controls in place.

The scope of a SOC 2 audit is something your organization defines. You choose which Trust Services Criteria apply to your business and which systems, products, or services fall “in scope.” A small startup might scope their audit narrowly around a single product. A larger healthcare technology company might scope it around their entire infrastructure, including subprocessors and third-party vendors.

Because SOC 2 is principles-based rather than prescriptive, you get flexibility in how you meet each criterion. The tradeoff is that your auditor still has to agree your chosen controls genuinely satisfy the criteria, so vague or weak controls won’t pass review just because you wrote a policy about them.

You might be thinking, “We already have HIPAA, why would we need SOC 2 too?” Here’s why SOC 2 compliance still matters even in a healthcare context:

For healthcare technology companies specifically, SOC 2 compliance automation tools have made this process far less painful than it used to be. Instead of manually collecting evidence for every control, automated platforms continuously monitor your systems and pull evidence in real time, which cuts audit prep from months down to weeks in many cases.

HIPAA stands for the Health Insurance Portability and Accountability Act. It was signed into law in 1996, and unlike SOC 2, it’s not optional. HIPAA was signed in 1996, with the parts that matter most for modern software companies arriving later through the Privacy Rule in 2003 and the Security Rule in 2005, which was last substantively updated in 2013.

Healthcare organizations face some of the highest cybersecurity stakes, with the average cost of a healthcare data breach reaching $7.42 million, while more than 167 million Americans had their healthcare information exposed in 2023 alone. These figures underscore why healthcare organizations need both strong regulatory compliance through HIPAA and robust security controls that frameworks like SOC 2 help demonstrate and validate.

In simple terms, HIPAA is the federal law that protects patient health information. If your organization creates, receives, stores, or transmits anything that counts as protected health information, or PHI, you are very likely subject to HIPAA, whether you’re a hospital, an insurance company, a billing service, or a software vendor that touches patient data in any way.

PHI is any health information that can identify an individual, and HHS defines 18 specific identifiers that, when combined with health information, make that information PHI. This includes things like names, dates of birth, medical record numbers, and even IP addresses when tied to health data.

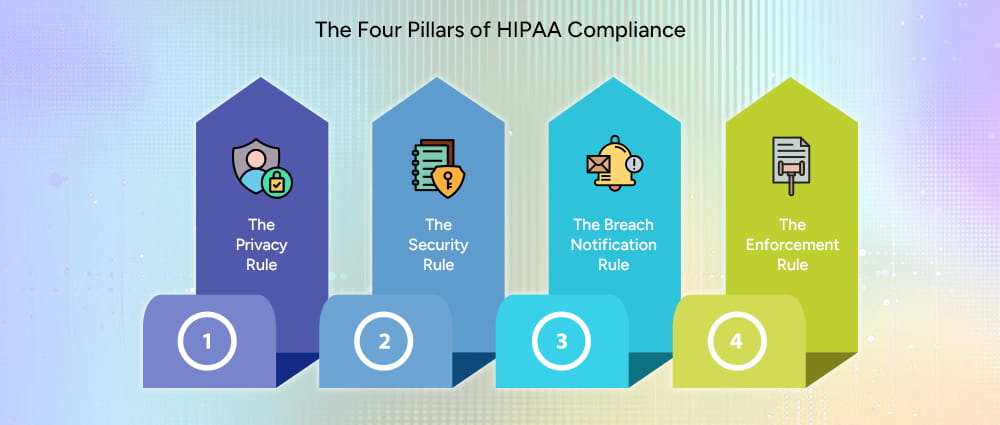

HIPAA is built around four core rules:

Unlike SOC 2, there’s no such thing as being “HIPAA certified.” You’re either compliant or you’re not, and you prove that compliance through documented policies, risk assessments, signed agreements, and audit-ready evidence rather than a single attestation report.

HIPAA exists to protect one of the most sensitive categories of personal data there is: a person’s health information. Before HIPAA, there were no consistent national standards for how that information had to be protected, which left patients vulnerable to having their medical history exposed, misused, or sold without any real accountability.

HIPAA’s scope is defined by who touches PHI, not by industry alone. Two types of organizations fall under its umbrella:

If your company is a business associate, HIPAA requires you to sign a Business Associate Agreement, or BAA, with every covered entity you work with. This agreement spells out exactly how you’ll protect PHI, what you’re allowed to do with it, and what happens if something goes wrong. There’s no equivalent requirement in SOC 2. This is one of the clearest dividing lines between the two frameworks.

One development worth watching closely if you’re building or scaling a healthcare software product: regulators have proposed tightening the HIPAA Security Rule considerably, removing the current distinction between “addressable” and “required” safeguards so that nearly everything becomes mandatory rather than optional. The proposed rule would also require AI tools to be included in risk analysis and risk management activities, which is a notable development for health AI startups. If finalized, this would raise the bar for HIPAA compliance for software development teams building AI-powered healthcare tools.

HIPAA isn’t just a regulatory checkbox. It directly impacts patient trust, legal exposure, and a healthcare technology company’s ability to operate at all.

This is exactly why so many healthcare technology companies turn to HIPAA compliance solutions and outside HIPAA compliance consulting early on, rather than trying to piece together a compliance program after they’ve already signed their first hospital client.

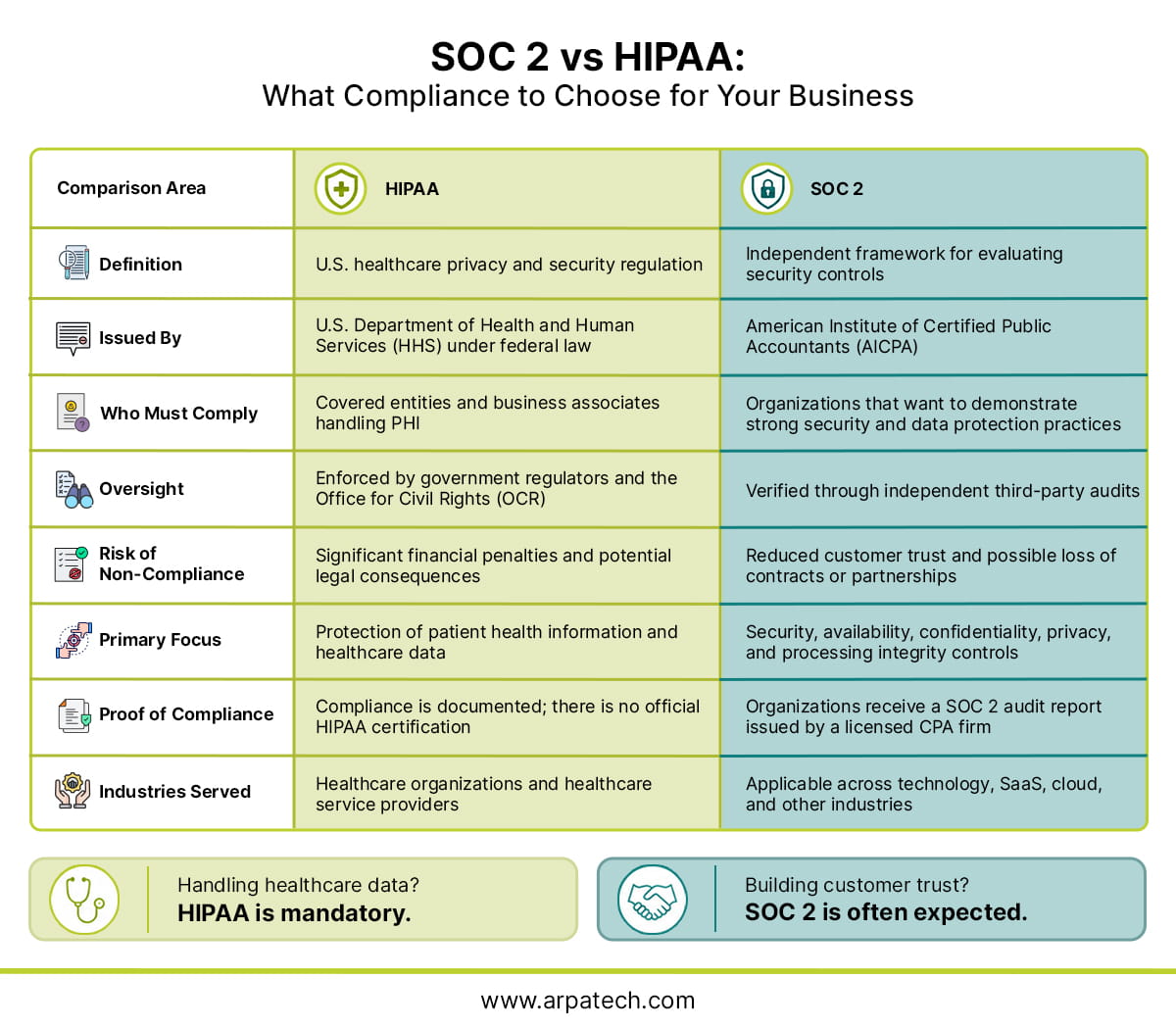

Let’s put the two side by side. Understanding these distinctions is the foundation of the entire SOC 2 vs HIPAA conversation.

Despite their different origins, SOC 2 vs HIPAA aim at a lot of the same underlying goals, and that overlap is exactly why combining them is more efficient than handling them separately.

Both frameworks care about:

Both frameworks also exist for the same fundamental reason: to give other people (whether that’s patients, business partners, or customers) confidence that an organization is handling sensitive data responsibly. Neither one is a static, one-time achievement. Both require ongoing monitoring, regular reassessment, and continuous evidence collection to stay valid over time, which is exactly the kind of work that HIPAA Compliance Automation and SOC 2 compliance automation platforms are designed to support.

For a lot of healthcare technology companies, the honest answer is yes. Here’s a simple way to think it through.

Ask yourself two questions:

If you answered yes to the first question, HIPAA compliance isn’t optional. It’s a legal requirement, and skipping it puts your company at serious financial and operational risk. If you answered yes to the second question, you’ll need SOC 2 to keep deals moving forward, regardless of whether you’re in healthcare or not.

If both apply, and for many healthcare SaaS companies, telehealth platforms, EHR systems, and patient engagement tools, both absolutely do apply, then you need both frameworks running side by side. The “good” news, if there is any, is that you’re not starting from zero twice. Because so many controls overlap between the two (access management, encryption, audit logs, risk assessments), building both programs together is significantly less work than building them one after the other.

Some companies genuinely only need one or the other:

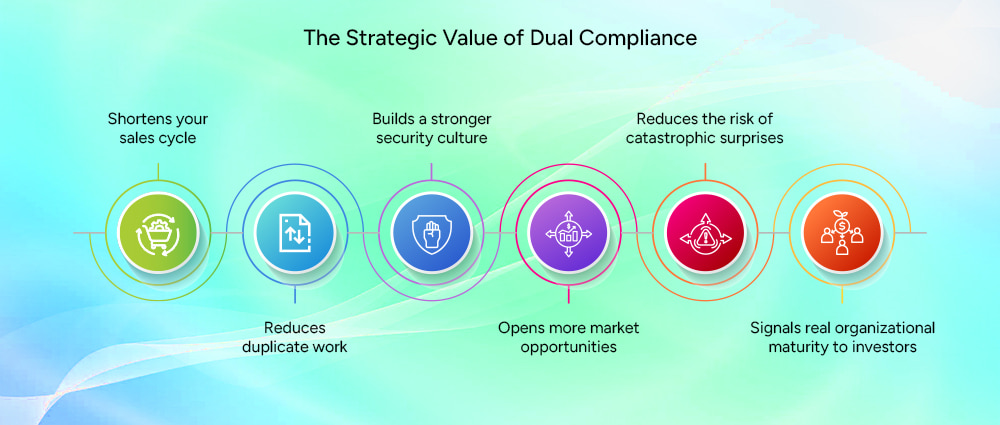

It’s easy to think of compliance as a cost center, something you do because you have to, not because it helps you. But pursuing SOC 2 and HIPAA compliance together can actually become a genuine competitive advantage for a healthcare technology company.

Here’s what dual compliance can do for your business:

The strategic upside is real, but only if the work is done thoughtfully. A rushed, checkbox-driven approach to either framework can leave you with a report or a policy binder that looks good on paper but falls apart the moment a real audit, breach, or regulator shows up.

So how do you actually decide what your company needs and how to get there? Here’s a practical way to approach it.

Start by mapping your data flows: Identify exactly where PHI enters, moves through, and exits your systems. If you can’t answer this clearly, that’s your first project, not your compliance audit.

Identify your regulatory obligations first, then your commercial pressures: HIPAA isn’t negotiable if you’re touching PHI. Figure that piece out before worrying about whether a prospect wants a SOC 2 report.

Decide on your SOC 2 scope carefully: Don’t just default to all five Trust Services Criteria. Most healthcare technology companies scope their SOC 2 around Security, with Confidentiality and Availability frequently added, and sometimes Privacy, depending on the nature of their product.

Build a control framework that serves both standards at once: Rather than building separate SOC 2 vs HIPAA programs, map your access controls, encryption standards, audit logging, incident response plans, and training programs so they satisfy both frameworks simultaneously wherever possible.

Decide between Type 1 and Type 2 for your SOC 2 report: If you’re early-stage and need something quickly to unblock a deal, Type 1 can work as a starting point. But most healthcare and enterprise buyers will eventually want to see Type 2, so plan your roadmap with that in mind from day one.

Invest in the right tools early: HIPAA Compliance Software and SOC 2 compliance automation platforms can dramatically reduce the manual burden of evidence collection, risk assessments, and continuous monitoring. Manually managing both frameworks with spreadsheets and shared drives becomes unsustainable fast, especially as your customer base and infrastructure grow.

Bring in outside expertise where it counts: A good HIPAA compliance consultant or GRC advisory partner can help you avoid the most common (and most expensive) mistakes: scoping your SOC 2 audit incorrectly, missing required BAAs with subcontractors, or building HIPAA policies that look complete but don’t hold up to real scrutiny from the Office for Civil Rights.

Treat compliance as continuous, not a one-time project: Both HIPAA and SOC 2 require ongoing maintenance. Controls need to be monitored, evidence needs to be refreshed, and your risk assessments need to evolve as your product, infrastructure, and customer base change.

This is especially important if your product involves AI in any way. Regulators are increasingly focused on how AI tools interact with PHI, and getting HIPAA compliance for software development right from the design phase, rather than retrofitting it later, will save you enormous pain down the road.

Figuring out the right path by differentiating between SOC 2 vs HIPAA doesn’t have to be something your team tackles alone, especially while you’re also trying to build and scale your actual product.

Arpatech’s Governance, Risk and Compliance Services are built specifically to help healthcare technology companies navigate exactly this kind of decision. Rather than treating compliance as an afterthought bolted onto your engineering roadmap, Arpatech’s GRCS advisory and consultation services help you build governance, risk management, and compliance into your business strategy from the ground up.

Here’s how that support typically plays out for healthcare technology companies:

If your healthcare technology company is trying to figure out whether you need SOC 2, HIPAA, or both, and you’d rather get expert guidance than guess your way through it, Arpatech’s Governance, Risk, and Compliance Services are built to help you make that call with confidence and build a compliance strategy that actually supports your growth instead of slowing it down.

As a SOC 2 Type 2 compliant organization, Arpatech understands firsthand what it takes to implement and maintain robust security controls, helping businesses navigate complex compliance requirements while strengthening trust and operational resilience.

SOC 2 vs HIPAA might get mentioned in the same sentence constantly, but they’re solving different problems. HIPAA is the law that protects patient health information and applies whether you like it or not, if you’re touching PHI. SOC 2 is the voluntary security attestation that proves to customers and partners that your broader security program is solid, tested, and trustworthy.

For a lot of healthcare technology companies operating in the US today, the real question isn’t SOC 2 vs HIPAA as an either-or choice. It’s how to build both into one coherent, efficient compliance strategy that protects patient data, satisfies your legal obligations, and keeps your sales pipeline moving. The overlap between the two frameworks means you don’t have to build everything twice, but you do need a clear strategy, the right HIPAA compliance solutions and SOC 2 compliance automation tools, and ideally, an experienced compliance partner who can help you avoid costly missteps along the way.

Getting this right isn’t just about avoiding penalties or checking a box for your next enterprise deal. It’s about building the kind of trust that lets healthcare organizations, patients, and partners feel confident handing you their most sensitive data. That trust, once you’ve earned it the right way, becomes one of the strongest assets your healthcare technology company has.

You don’t have to map out your SOC 2 vs HIPAA strategy on your own. If you want an expert second opinion on where your healthcare technology company actually stands, or you’re ready to build a compliance roadmap that won’t slow your growth down, reach out to Arpatech for a one-on-one consultation. Their Governance, Risk, and Compliance team can walk through your specific product, data flows, and customer requirements, and help you figure out exactly what SOC 2 and HIPAA compliance should look like for your business, before a deal or an audit forces the question for you.

Let’s get your SOC 2 vs HIPAA compliance straight!

Ramsha Khan

Jun 30, 2026

Automating Healthcare Revenue Cycle Management: Process...

Running a hospital, clinic, or healthcare organization involves complicated financial tasks, not just clinical challenges. Every time a patient interacts with staff, it starts a series of administrative and billing processes. If these processes are not handled well, the organization can lose revenue, face delays in getting paid, and experience cash flow issues. According to the American Hospital Association, hospitals used $43 billion in 2025, trying to collect payments from insurers for care already provided, with nearly $18 billion spent on fighting denied claims.

Automating healthcare revenue cycle management is essential for providers today. They face many challenges, such as changing payer requirements, new compliance regulations, rising claim denials, and labor shortages. At the same time, there is pressure to cut administrative costs while still delivering quality care. Without an efficient revenue cycle in place, even the best healthcare organizations may struggle financially. And without automating processes, they are collapsing under pressure.

Every time a patient visits, there is a financial process behind it, and healthcare revenue cycle management keeps this process running smoothly. It involves how healthcare providers collect patient information, check insurance, submit claims, and collect payments. According to Experian Health’s State of Claims 2025, 41% of providers say that at least one in ten of their claims gets denied.

This shows that having a strong revenue cycle is important, and automating the healthcare system is even more important, not only for daily operations but also as a financial safety measure. Automating healthcare revenue cycle management helps providers reduce administrative burdens, improve cash flow, minimize denials, and deliver a better financial experience for patients.

When the system works well, organizations have healthy profits and can invest more in patient care. However, when it fails, staff become overwhelmed, revenue slows down, and leaders lose track of their finances.

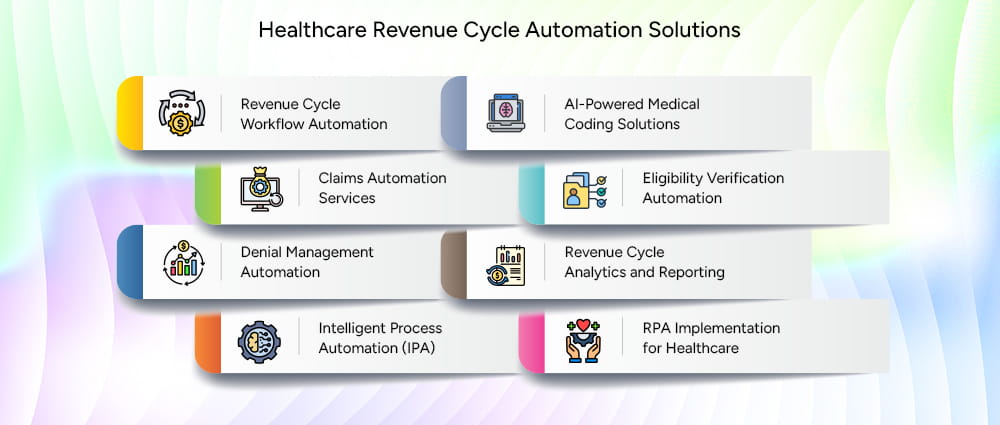

Whether you are exploring healthcare revenue cycle automation solutions for the first time or looking to optimize existing workflows, understanding how each stage of the revenue cycle can be streamlined through automation is the first step toward improving financial performance and operational efficiency.

In this blog, we cover:

If we talk about what is revenue cycle management in healthcare, it refers to the end-to-end process of managing the financial lifecycle of a patient encounter from the moment an appointment is scheduled to the moment payment is fully collected and reconciled.

It encompasses clinical, administrative, and financial functions that work together to ensure that healthcare services are accurately billed and appropriately reimbursed.

Healthcare revenue cycle management ensures providers get paid the right amount, at the right time, for the care they deliver. This involves verifying patient eligibility, assigning the correct medical codes, submitting clean claims to payers, following up on unpaid or denied claims, and collecting patient balances.

It also involves financial reporting and analytics that give leadership insight into where revenue is being lost and how performance can be improved.

Healthcare RCM is complicated because it brings together so many different parties under one process: patients, providers, payers, and government programs like Medicare and Medicaid, each playing by its own rules and timelines. One coding error, a missing document, or a submission mistake can be enough to trigger a denied claim, delay a payment, or create a compliance issue. It is no surprise then that healthcare revenue cycle management has grown into a specialized field that requires deep industry knowledge and the right technology to get it right.

Today, automation in healthcare is transforming how providers manage these complexities. Through healthcare workflow automation, business process automation, and AI-driven tools, organizations can streamline repetitive administrative tasks, improve coding accuracy, and accelerate reimbursements.

Technologies such as automated claims processing, predictive analytics, and AI agents in healthcare are helping providers reduce manual workloads, minimize claim denials, and create a more efficient and financially sustainable revenue cycle.

Understanding how the healthcare revenue cycle works requires looking at each stage as an interconnected workflow. A breakdown at any point can affect everything downstream.

Today, automation in healthcare helps providers streamline these processes, improve accuracy, and reduce administrative burdens.

The revenue cycle starts at scheduling, long before a patient sees a medical professional. Demographic and insurance details are collected and entered into the system, and accuracy here is critical. A simple error in a name, date of birth, or insurance ID can trigger claim rejections weeks later. Any prior authorizations required by the payer are also secured at this stage.

Many healthcare enterprises use healthcare workflow automation and business process automation tools to simplify scheduling and reduce manual data entry.

Patient calls or visits → appointment scheduled → demographic and insurance details collected → prior authorizations obtained where applicable.

After registration, providers must confirm that the patient’s plan is active and the planned services fall within their coverage. This step, known as eligibility verification, determines what the payer will cover, which deductibles apply, and what the patient owes.

Rushing through it is one of the fastest ways to invite claim denials. Efficient healthcare organizations have built real-time eligibility checks and automated workflows into their scheduling process as a matter of course.

Insurance details submitted → real-time eligibility check run → coverage confirmed → deductibles and patient responsibility identified → authorization gaps flagged.

After a patient visit, healthcare providers record the services provided, diagnoses made, and procedures performed. Medical coders then turn that information into standard codes, using ICD-10 for diagnoses and CPT for procedures. Getting the coding right is important because if the billing is too low, the practice loses money, and if it’s too high, there might be compliance issues.

Charge capture ensures that every service offered is included before the claim is sent to the insurance company. Increasingly, AI agents in healthcare are assisting with coding accuracy and identifying missing documentation.

Patient visit ends → provider records services, diagnoses, and procedures → medical coder assigns the right codes → charge capture checks that nothing is missed → claim is prepared and sent for submission.

Once coding is completed, the billing team sends the bill to the right payer. Before it gets there, the claim is reviewed for formatting and coding errors. The payer then looks at the provider’s contract, the patient’s coverage, and the claim itself to decide how much to pay.

A clean claim gets processed quickly, while one with errors gets sent back, costing the organization both time and money. Automated claims processing and business process automation help providers validate claims and accelerate reimbursements.

Bill prepared → sent for error review → formatting checked → clean claim forwarded to payer → payer reviews and decides payment amount.

When a payer processes a claim, they send a payment summary that explains what was paid, what was adjusted, and what was denied. Payment posting is the process of recording these payments in the provider’s accounting system and checking them against expected amounts.

This step is essential for keeping finances accurate and for spotting issues with underpayments or contractual adjustments that may need attention. Healthcare workflow automation helps organizations improve efficiency and maintain accurate financial records.

Payer sends payment summary → payment amount reviewed → payments recorded in accounting system → compared to expected amounts → any underpayments or adjustments marked for follow-up.

Claims do not always get paid on the first submission. Missing information, coding errors, medical necessity disputes, coverage limitations, and other issues can lead to denials. Managing them effectively comes down to monitoring rejections by type and payer, understanding why they happened, fixing the issue, and resubmitting without delay.

Appeals are filed when the situation calls for it. Organizations that leverage automation in healthcare, predictive analytics, and AI agents in healthcare can identify denial patterns earlier and recover more revenue than those that write denials off.

Claim denied → reason identified → issue fixed or extra documents gathered → claim resubmitted or appeal filed → payment recovered or written off.

Modern healthcare revenue cycle management depends on more than billing systems alone. Today, automation in healthcare is driven by intelligent technologies that streamline repetitive processes, reduce manual errors, and improve financial performance. From business process automation to AI-driven analytics, these technologies are transforming how providers manage the revenue cycle.

In Healthcare revenue management cycle, business process automation platforms help healthcare organizations standardize repetitive tasks such as patient registration, eligibility verification, prior authorizations, payment posting, and denial management.

By automating these workflows, providers can improve efficiency while minimizing manual errors and administrative burdens. As healthcare organizations scale, business process automation enables teams to maintain consistent workflows while accelerating reimbursements and reducing operational costs.

Automated claims processing has become one of the most valuable technologies in modern revenue cycle management. These solutions perform claim scrubbing, error detection, and electronic submission to ensure claims are complete before reaching payers.

Automated systems can identify coding inconsistencies, flag missing information, and streamline remittance posting after payments are received. By reducing manual intervention and preventing avoidable errors, automated claims processing helps organizations improve first-pass claim acceptance rates and shorten reimbursement cycles.

AI agents in healthcare are bringing a new level of intelligence to revenue cycle operations. Powered by generative AI, natural language processing (NLP), and predictive analytics, these systems can automate repetitive tasks, uncover hidden patterns, and improve financial performance.

By reducing administrative workloads, AI agents allow staff to focus on higher-value activities while enhancing efficiency across the revenue cycle.

Key applications of AI agents in healthcare include:

Healthcare workflow automation platforms connect clinical, administrative, and financial processes across the organization. Through workflow orchestration, EHR integration, and billing system integration, these platforms enable data to move seamlessly between departments without manual intervention.

Healthcare workflow automation eliminates duplicate data entry, improves collaboration, and ensures that information flows efficiently throughout the revenue cycle. By creating a connected ecosystem, healthcare organizations can improve productivity, enhance accuracy, and deliver a more efficient experience for both staff and patients.

As healthcare organizations continue to modernize, automation in healthcare is helping providers improve financial performance while reducing administrative complexity. Through healthcare workflow automation, business process automation, and healthcare revenue cycle management software, organizations can streamline operations, reduce errors, and create better experiences for both staff and patients.

Many healthcare revenue cycle management companies and healthcare revenue cycle management services now leverage these technologies to deliver more efficient and scalable solutions.

Healthcare workflow automation helps organizations connect clinical, administrative, and financial processes, leading to smoother operations and improved coordination.

Healthcare automation reduces the need for manual data entry and repetitive tasks, allowing staff to focus on higher-value work.

Automated claims processing helps providers identify errors before submission, improving first-pass claim acceptance rates and reducing lost revenue.

Business process automation enables healthcare organizations to standardize workflows and eliminate bottlenecks. AI agents in healthcare can further support coding, claims review, and denial management.

Modern healthcare revenue cycle management solutions accelerate claims processing and payment posting, resulting in healthier cash flow.

An efficient revenue cycle benefits patients as much as providers. AI agents in healthcare and automated communication tools help create a more transparent billing experience.

Ultimately, what is revenue cycle management in healthcare is evolving beyond traditional billing. With the help of healthcare revenue cycle management software and intelligent automation, providers are creating more efficient, scalable, and patient-centered financial operations.

Many providers are now adopting healthcare revenue cycle management solutions that combine automation in healthcare, AI, and intelligent workflows to improve efficiency and financial performance.

Whether delivered through healthcare revenue cycle management software or specialized healthcare revenue cycle management services, these technologies help organizations streamline operations while reducing administrative burdens.

Healthcare workflow automation connects clinical, administrative, and financial processes to eliminate bottlenecks and improve coordination across the revenue cycle.

From patient registration to payment posting, automated workflows help providers increase efficiency and reduce manual errors.

AI agents in healthcare are transforming medical coding through natural language processing (NLP) and intelligent automation.

These solutions help coders improve accuracy, accelerate claim preparation, and reduce compliance risks while minimizing the need for manual intervention.

Automated claims processing enables providers to streamline claim scrubbing, electronic submission, error detection, and remittance posting.

By identifying issues before claims reach payers, organizations can improve first-pass acceptance rates and accelerate reimbursements.

Insurance verification is one of the most repetitive stages of revenue cycle management healthcare operations.

Through business process automation, providers can perform real-time eligibility checks, identify authorization gaps, and reduce the risk of denied claims before treatment begins.

Advanced healthcare revenue cycle management companies are using predictive analytics and AI agents in healthcare to identify denial patterns and prioritize claims that require immediate attention.

Automated workflows help organizations recover revenue faster and improve collections.

Analytics and reporting automation testing tools provide real-time visibility into key performance indicators such as denial rates, collection rates, and days in accounts receivable.

These insights help leadership identify inefficiencies and optimize financial outcomes.

Intelligent Process Automation (IPA) combines artificial intelligence, machine learning, and business process automation to manage complex workflows that traditionally required human intervention.

By integrating data and decision-making capabilities, IPA enables healthcare organizations to scale operations while maintaining accuracy and compliance.

Robotic Process Automation (RPA) allows healthcare organizations to automate repetitive administrative tasks such as appointment scheduling, eligibility verification, claims processing, and payment posting.

As healthcare automation continues to evolve, RPA is becoming an essential component of modern healthcare revenue cycle management software and digital transformation initiatives.

Choosing the right healthcare revenue cycle management service provider has lasting financial consequences. Here is what to look for:

The cost of healthcare revenue cycle management depends on the technologies and resources used to support the process. As organizations adopt healthcare revenue cycle management solutions, understanding the main cost drivers can help maximize long-term value.

Labor remains one of the largest expenses in revenue cycle management healthcare operations. Salaries for billing specialists, coders, denial management teams, and revenue cycle leaders, along with ongoing training, can significantly impact operating costs.

Healthcare revenue cycle management software requires investment in:

Denied claims create hidden expenses through:

Healthcare automation technologies may require upfront investment, including:

Healthcare revenue cycle management services and healthcare revenue cycle management companies typically charge 3% to 8% of collections, depending on the provider’s size and specialty.

Although automation in healthcare requires initial investment, organizations often achieve long-term savings through:

By leveraging business process automation and AI agents in healthcare, providers can build more efficient and scalable revenue cycle operations.

Even well-resourced healthcare organizations face persistent challenges in managing their revenue cycles effectively.

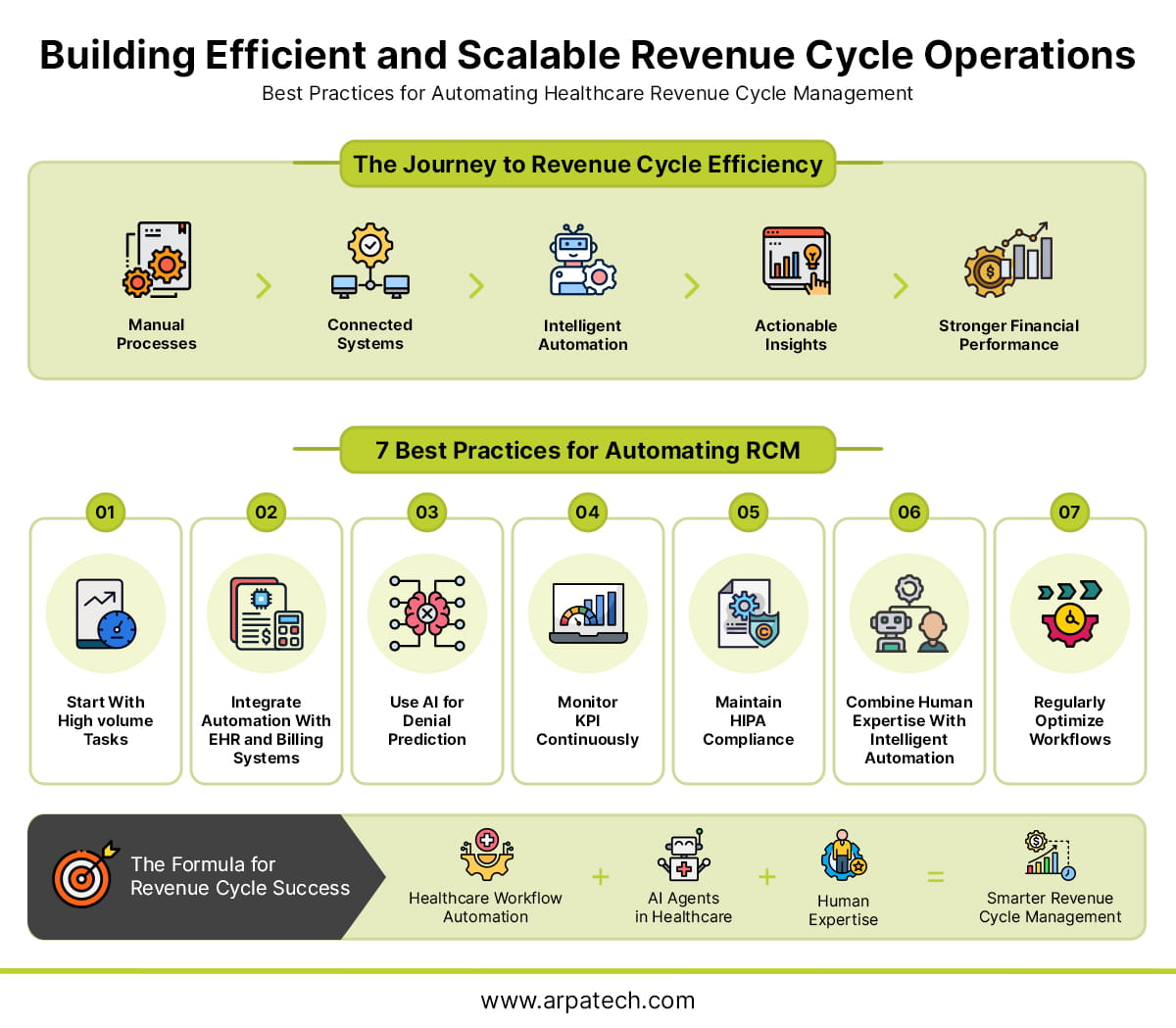

Organizations that achieve the greatest success with healthcare revenue cycle management solutions take a strategic approach to healthcare automation. The following best practices can help providers improve efficiency, reduce denials, and maximize financial performance.

Automation in healthcare delivers the most value when applied to routine processes that consume significant time and resources.

Focus on automating:

Healthcare workflow automation works best when clinical and financial systems are connected. Seamless EHR and billing system integration reduces duplicate data entry, improves accuracy, and accelerates reimbursement cycles.

AI agents in healthcare and predictive analytics can identify high-risk claims before submission, allowing organizations to address issues proactively rather than recovering revenue after denials occur.

Successful healthcare revenue cycle management companies rely on data-driven decision-making. Key metrics to monitor include:

As healthcare revenue cycle management software becomes increasingly automated, organizations must ensure that workflows, data storage, and system integrations remain secure and compliant with HIPAA requirements.

Business process automation and automated claims processing are most effective when paired with skilled staff. Intelligent technologies should enhance human decision-making, not replace it entirely.

Healthcare automation is an ongoing process. Organizations should continuously evaluate performance, refine workflows, and adopt new technologies to keep pace with changing payer requirements and industry demands.

By combining healthcare workflow automation, AI agents in healthcare, and business process automation with experienced teams, providers can build more efficient, scalable, and financially resilient revenue cycle operations.

Healthcare revenue cycle management ranks among the most vital operational functions in any provider organization. When it runs well, it supports financial stability, keeps operations efficient, automates workflows, and allows providers to focus on delivering quality care without constant financial pressure. When it breaks down, the effects show up across the entire organization, in staffing decisions, technology investments, and the ability to serve patients effectively.

Organizations that combine strong processes with modern healthcare revenue cycle management solutions, automated claims processing, and AI agents in healthcare are building more efficient and resilient revenue cycle operations. As automation in healthcare continues to advance, providers who embrace intelligent workflows today will be better positioned for long-term success.

Ready to modernize your revenue cycle? Connect with Arpatech to discover how our healthcare revenue cycle management services and automation solutions can help streamline operations and accelerate growth.

The healthcare revenue cycle management software market offers options for all organizational sizes, from large companies like Epic and Cerner to mid-size solutions like Kareo and Athenahealth.

When selecting software, consider how well it integrates with EHR systems, how it handles denial management, and the support from the vendor. No platform delivers results on its own. The organizations that get the most out of their software are the ones that back it up with experienced outsourced RCM expertise.

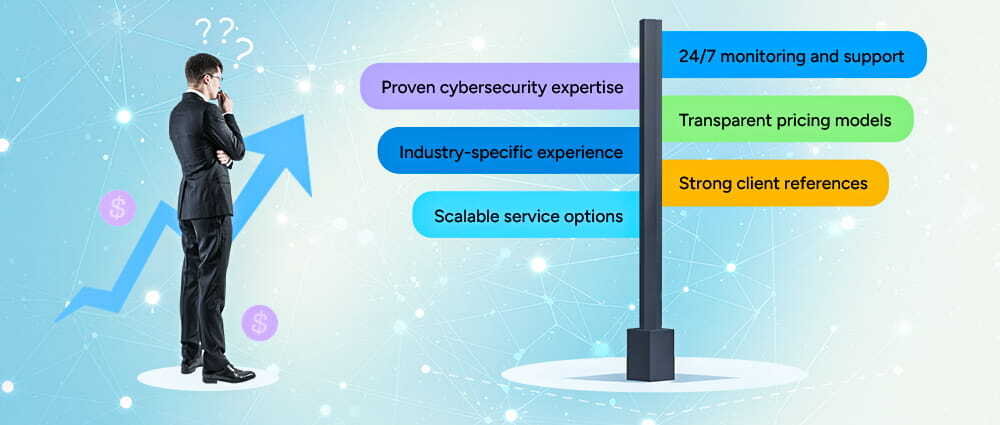

Identify your biggest challenge first: coding accuracy, denial rates, or eligibility gaps. Find a provider whose strengths match your challenge. Ask for first-submission acceptance rates and denial resolution timelines from the start so you have a clear basis for comparison. Next, look at how they communicate and handle performance reporting. Good partners are transparent, proactive, and easy to work with. Confirm HIPAA compliance, data security, and payer experience, and ask for references from organizations of a similar size and specialty before making a final decision.

Building a strong medical billing team from scratch takes time and money, most healthcare organizations do not have. Outsourcing gives them immediate access to trained coders, established payer relationships, and proven workflows that deliver cleaner claims, faster reimbursements, and fewer denials.

On top of that, it eases the burden on internal staff, reduces the disruption of team changes, and keeps pace with organizational growth. Clinical teams stay where they are needed most while experienced partners handle the revenue cycle day to day.

Go beyond marketing claims when evaluating healthcare revenue cycle management companies. Case studies, client testimonials, and directories from organizations like the Healthcare Financial Management Association are good starting points, keeping in mind that hospital systems, outpatient clinics, and specialty practices each have different RCM needs.

Ask for proposals that include performance guarantees, reporting methods, and pricing structures. Good providers have no problem showing how they measure success and pointing to real improvements in days in AR, net collection rates, and denial rates across their client portfolio.

By removing manual steps from error-prone processes, automation makes healthcare revenue cycle management faster and more reliable. Real-time eligibility verification, automated claim validation, and remittance posting each take a layer of human error out of the equation before it becomes a problem.

Advanced analytics and AI bring an added layer of intelligence to the process, helping organizations predict which claims may face rejection, catch documentation gaps early, and better understand payer behavior to build stronger appeals. Organizations that invest here pull ahead of peers across every major RCM metric while reducing administrative costs and letting staff concentrate on work that needs their attention most.

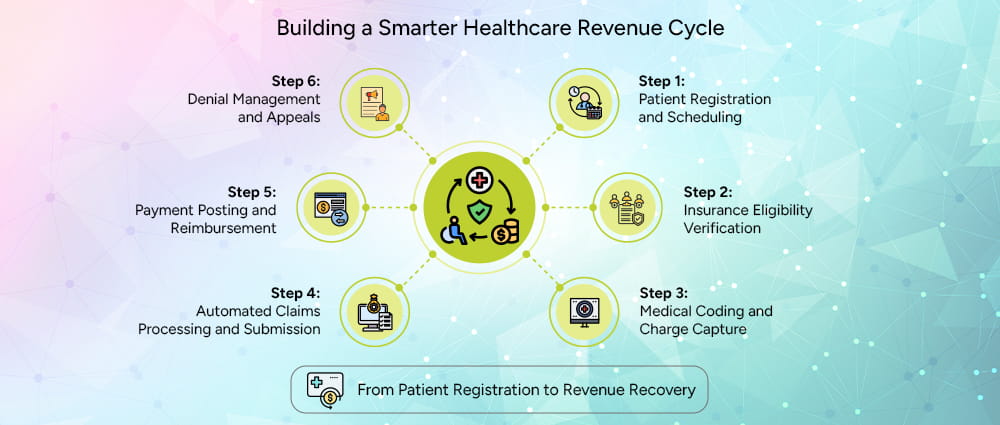

The healthcare revenue cycle moves through six stages: patient registration, eligibility verification, medical coding and charge capture, claims submission, payment posting, and denial management. They are deeply connected, and when one breaks down, the rest feel it. That interconnection is what makes investing in the right healthcare revenue cycle management solutions so important for any healthcare organization.

Ramsha Khan

Jun 17, 2026

In-House vs. Managed SOC: A CISO’s Decision Frame...

If you’re a CISO or a senior security leader in 2026, there’s a good chance you’ve sat in a budget meeting recently and had to answer a very uncomfortable question: “Do we really need to build our own Security Operations Center, or should we just outsource it?”

It’s not a simple question.

The pressure coming from every direction has never been more intense. Ransomware attacks are faster and more automated than ever. The CrowdStrike 2026 Global Threat Report documented an average attacker breakout time of just 29 minutes in 2025, meaning that’s how long it takes a threat actor to move from initial access to lateral movement across your systems.

That’s not a comfortable margin. And with AI-powered attacks now automating the early stages of intrusion, that window is only going to keep shrinking, which is why we need governance and risk management.

At the same time, the talent market is a disaster. The global cybersecurity staffing gap has reached 4.8 million unfilled positions according to ISC2’s latest workforce study, with over 500,000 of those vacancies sitting in the United States alone. Regulatory requirements are tightening. Budgets are being scrutinized like never before. And you’re expected to deliver 24/7 protection while somehow keeping everyone on your team from burning out and walking out the door.

So the in-house vs. managed SOC debate is no longer purely philosophical. In 2026, it’s one of the most consequential operational decisions a security leader will make.

This guide walks CISOs through the real cost comparison, talent challenges, compliance considerations, and a practical decision checklist for choosing the right SOC model in 2026

Before diving into the comparison, it’s worth grounding the conversation for any stakeholders who may not live in this world every day.

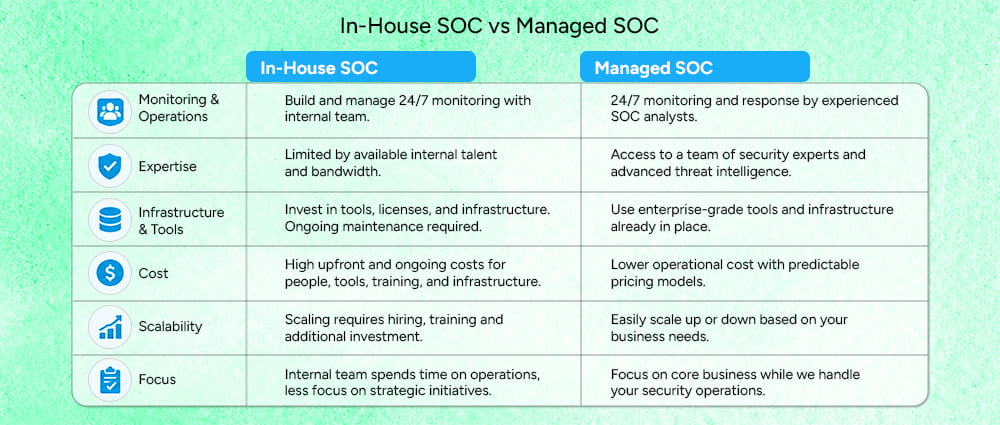

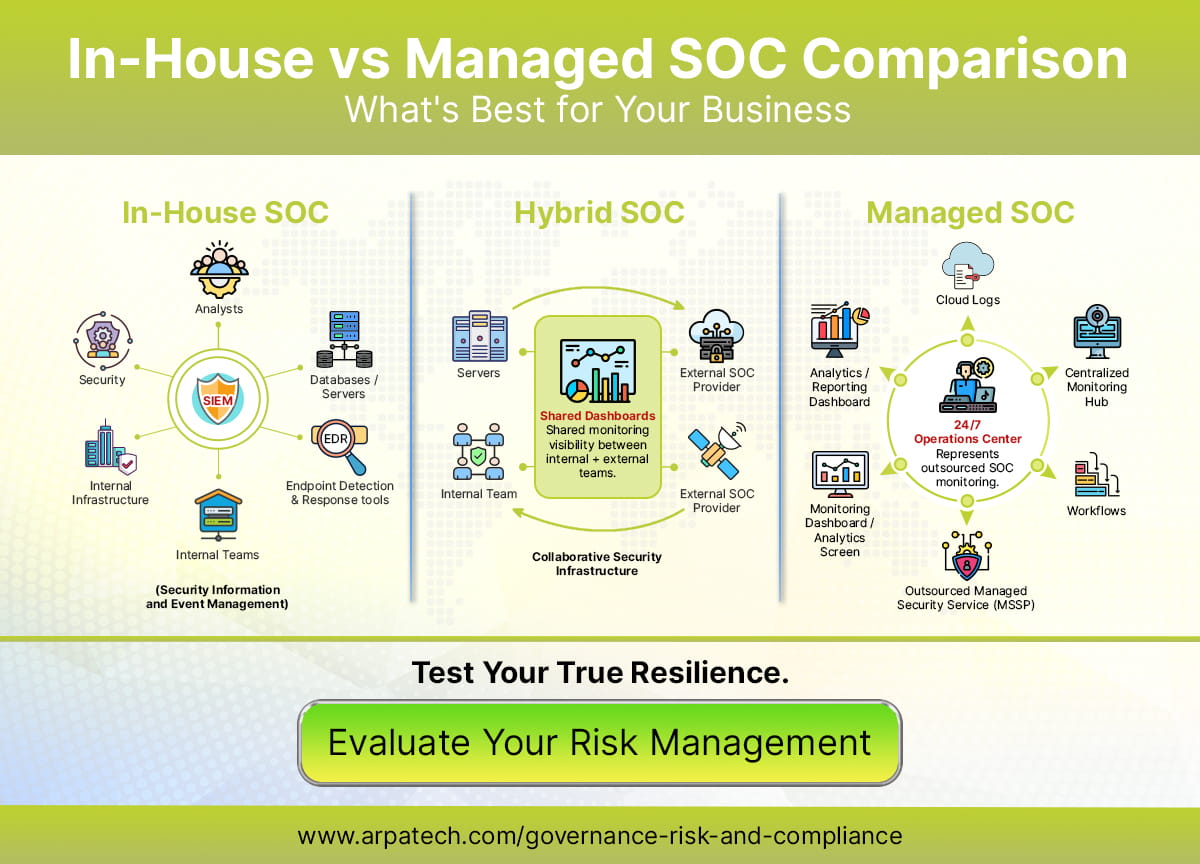

A security operations center (SOC) is a centralized function: either a physical team room or a virtual capability, staffed by security analysts who monitor, detect, investigate, and respond to cybersecurity threats around the clock. A SOC is the operational nerve center of your security program. It’s where SIEM alerts get triaged, where incident response kicks off, where threat hunters look for adversary behavior that automated tools might miss, and where your compliance monitoring gets turned into actionable intelligence.

The core tools inside a SOC typically include a Security Information and Event Management (SIEM) platform, Security Orchestration, Automation and Response (SOAR) capabilities, Endpoint Detection and Response (EDR) or Extended Detection and Response (XDR), and network detection tools. Managing all of this, and keeping it staffed is the operational challenge that makes the build vs. buy question so relevant.

A managed SOC, sometimes called SOC as a service or security operations center as a service, is essentially what it sounds like: you engage a third-party managed security services provider (MSSP) who brings their own analysts, tools, infrastructure, and processes to monitor and protect your environment. You get the output of a fully staffed SOC without having to build or staff one yourself.

The question every CISO has to answer is which approach actually makes more sense for their specific organization in 2026.

The Numbers Nobody Puts in the First Slide.

Let’s start with what it actually costs to build and operate your own security operations center, because internal budget proposals almost always undercount the true total.

The highest cost in running a SOC is people.

To truly operate 24/7, you need three shifts every day of the week. You also need extra staff to cover sick days, vacations, and training. This means building a fairly large team just to keep monitoring continuously and reliably.

Then comes the technology. A modern SOC depends on multiple security tools working together, along with the infrastructure needed to run them. As your environment grows, the effort and expense to maintain these tools also grow.

Recruiting and training are often overlooked. Hiring and preparing security analysts takes time, effort, and resources. On top of that, many SOC analysts leave their jobs after a short period due to burnout. This means you are frequently replacing team members, and each departure takes valuable experience and knowledge with it.

The all-in number for a mid-sized organization building a true in-house SOC lands between $1.2 million and $2.5 million per year. Enterprise-level operations with more complex environments can run $4 million or more annually when you factor in everything.

Managed SOC services in 2026 are priced primarily on a subscription model, typically based on the number of endpoints monitored, the volume of data ingested, or user counts, depending on the provider’s model.

For organizations with 200 to 2,000 employees, market pricing generally runs between $5,000 and $25,000 per month, or $60,000 to $300,000 annually. For a mid-market company, this translates to roughly $120,000 to $720,000 per year, depending on scope, endpoint count, and compliance requirements.

The bottom line on cost comparison: managed SOC services tend to cost 30 to 50 percent less than building a comparable in-house SOC, once staffing, tooling, and turnover costs are fully accounted for. A 2026 analysis of mid-sized organizations found that managed SOC services cost approximately $630,000 to $965,000 less annually than in-house operations. Organizations implementing outsourced managed security services have reported saving an average of $2.22 million compared to maintaining internal security teams.

Those are not small numbers.

The cost advantage of managed SOC is compelling on its own. But in 2026, the talent problem is just as important, and it’s getting worse, not better.

The numbers tell a brutal story. The global cybersecurity workforce would need to nearly double just to fill every open role today. That’s not a rounding error; it’s a structural crisis that’s been building for years and shows no signs of slowing down.

What’s making it worse is that the hiring barrier has shifted. It’s no longer just about finding qualified people. Budget cuts have now become the bigger obstacle, meaning many organizations have the job postings ready but simply can’t afford to pay what the market demands. They want to hire. They just can’t.

And the consequences are showing up in real incidents. According to the 2026 SANS/GIAC Cybersecurity Workforce Research Report, 88% of organizations experienced a significant security incident in the past year that they directly tied to not having enough skilled people on staff. The skills gap isn’t an HR problem anymore. It’s a security failure waiting to happen.

Then there’s burnout, and inside SOC teams, it’s a crisis of its own. According to Sophos research, here’s what the average SOC team looks like right now:

What does this mean practically? Even if you successfully build your SOC team, you’re essentially managing a revolving door. You’re constantly recruiting. You’re losing institutional knowledge every time someone walks out.

And in a competitive labor market, a larger organization with a bigger brand and a higher salary budget can simply outbid you for the same candidates.

A managed security services provider operates differently. Their scale lets them attract, develop, and retain analysts in ways a single mid-sized business simply can’t match.

Those analysts work across dozens of client environments, which means they’re exposed to a wider range of attack scenarios and threat patterns than any in-house team would typically see.

The practical result is that the analyst quality you get through a managed engagement is often higher than what you could realistically hire and keep on your own.

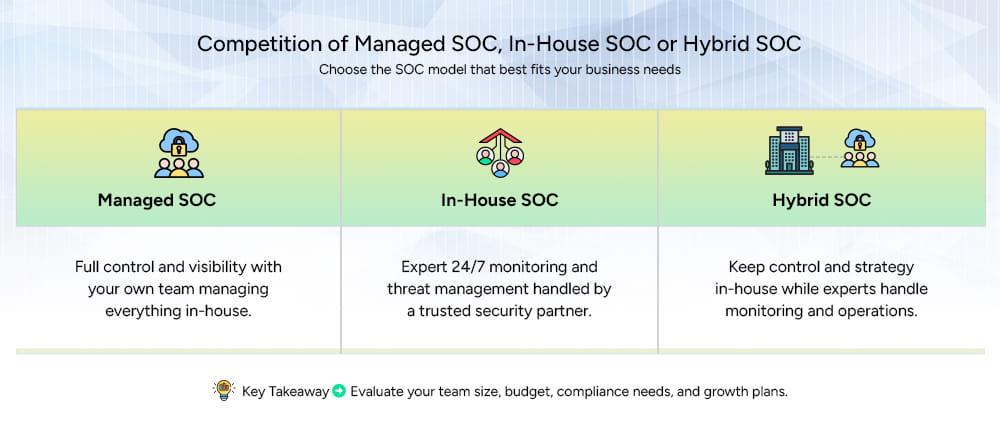

To be fair to the other side of the argument, because this is a CISO’s decision framework, not a managed SOC sales pitch, there are real scenarios where building in-house makes sense.

If you’re operating at a scale where you can sustain the headcount, the tool spend, and the leadership infrastructure, an in-house SOC gives you maximum control, full customization of detection logic, and the ability to build institutional knowledge that’s deeply tailored to your environment.

Defense contractors, certain government agencies, and organizations dealing with classified data sometimes face constraints that make third-party access to their environments impractical or legally prohibited. In those cases, you don’t really have a choice: you build in-house.

If you have a strong Director of Security Operations and an established detection engineering capability, you may be past the tipping point where building makes more sense than buying. The investment has already been made in people and process.

Some organizations have such unique environments: bespoke industrial systems, highly specialized regulatory requirements, or niche technology stacks, that a generalist managed provider simply can’t deliver the detection depth you need.

Outside of these scenarios, however, the calculus for most mid-sized US organizations has shifted considerably toward managed SOC services.

Rather than making this a pure cost comparison, here’s how to think through the full set of considerations that should drive your decision.

A two-hour gap in analyst coverage on a Saturday night isn’t a compliance problem: it’s how a contained incident becomes a breach. True 24/7 monitoring requires significant headcount and shift scheduling that most mid-sized organizations struggle to sustain. Managed SOC providers operate under SLA commitments, typically promising a response within 15 to 60 minutes, depending on severity. And because they’re monitoring your environment with AI-assisted tooling and cross-client threat intelligence, they often detect threats faster, even with that SLA window.

Managed security services increasingly include compliance automation capabilities that address frameworks like SOC 2, HIPAA, CMMC, and others. Organizations with managed SOC coverage typically see 15 to 30% reductions in cyber insurance premiums, partly because carriers are increasingly requiring evidence of 24/7 SOC monitoring as a baseline policy condition. The compliance lift from a managed provider can be substantial, and often more defensible in an audit than a self-attested in-house program.

An in-house SOC typically requires 6 to 18 months to reach operational maturity. That’s 6 to 18 months of exposure during a period when you’re building processes, tuning detection rules, and getting your analysts up to speed. Managed SOC providers come pre-built. Most can onboard a new client in 30 days or less.

If your organization is growing, expanding into new cloud environments, or making acquisitions, a managed SOC can scale with you without requiring you to hire and train new analysts every time. An in-house SOC is somewhat rigid: scaling up means a hiring cycle that could take months.

This is a legitimate concern with managed providers. How much visibility do you get into what they’re actually doing? The better providers offer full investigation transparency, observable actions, and regular reporting that gives you genuine insight into your security posture.

When evaluating a managed security services SOC provider, transparency into detection logic and incident workflow should be a non-negotiable requirement.

It’s worth noting that the choice isn’t always binary. Many mid-sized organizations in 2026 are running a hybrid model: a small internal team handles governance, compliance oversight, strategic risk management, and vendor oversight, while the managed provider covers 24/7 monitoring and response.

This isn’t a compromise: it’s often the most practical model for organizations that have outgrown a purely reactive posture but can’t justify the headcount for a full internal SOC. According to recent industry data, 43% of organizations now outsource parts of their security operations. The managed layer adds capacity and specialized capability where the internal team has gaps, without giving up all strategic ownership.

The hybrid approach works particularly well when:

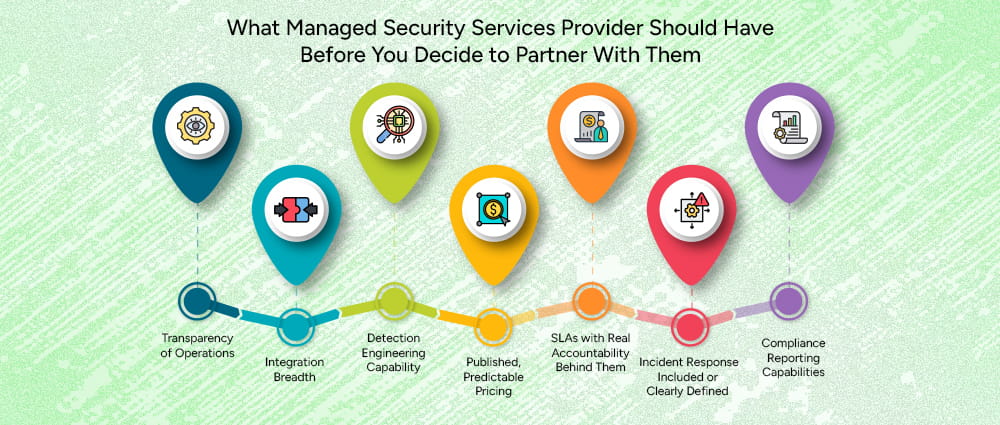

If you’re leaning toward managed SOC services, the provider selection process matters enormously. The market has become crowded, and not every provider delivers what it promises. Here’s what to vet rigorously:

Can you see what your analysts are doing, what alerts they’re prioritizing, and how they’re resolving incidents? Opacity is a red flag. You need to be able to see the entire process.

A good managed security services provider should be able to integrate with your existing tool stack, not require you to rip and replace everything. Look for vendors with broad integration libraries.

Are they doing custom detection work for your environment, or just applying a generic ruleset? The best providers tune detection logic during onboarding.

Hidden ingestion fees and per-ticket charges can turn a seemingly affordable contract into a budget problem. Demand transparent pricing before you sign.

Mean time to detect (MTTD) and mean time to respond (MTTR) should be contractually committed, not just aspirational.

What happens when something major occurs? Do they have an IR team, or do they just hand you a report and wish you luck?

If you’re in a regulated industry, confirm that their reporting outputs actually map to your framework requirements.

One of the hardest parts of this conversation for CISOs is making the financial case internally. Here’s how to frame it.

The global average cost of a single data breach reached $4.44 million in 2025. In the United States, that number climbed to $10.22 million. Organizations with significant security staffing shortages pay nearly $2 million more per breach than well-staffed peers. Meanwhile, organizations that make extensive use of security AI and automation- the kind that’s embedded in modern managed SOC platforms- save an average of $2.2 million in data breach costs and identify and contain breaches nearly 100 days faster.

A managed SOC that prevents even one major incident pays for itself multiple times over.

There’s also the insurance angle. Cyber insurers are increasingly requiring evidence of 24/7 SOC monitoring, documented incident response capability, and measurable MTTD/MTTR as baseline underwriting conditions. Organizations with managed SOC coverage typically see 15 to 30% premium reductions. The cost savings on insurance alone can offset a meaningful portion of a managed SOC contract.

Here’s a practical checklist to help you organize your thinking:

In 2026, the question isn’t whether your organization needs a security operations center. The threat environment has settled that debate. The question is which operating model actually reduces risk, fits your budget, and gives you the resilience to sustain security operations over time: not just during a good staffing year.

For most mid-sized US organizations, managed SOC services deliver faster detection, more consistent response, lower operational burden, predictable costs, and fewer security blind spots. The talent market is too difficult, the burnout rates are too high, and the cost differential is too significant to ignore.

That’s where a partner like Arpatech comes in. For organizations that need more than just monitoring, Arpatech’s Governance, Risk, and Compliance (GRC) services help security leaders build the structural foundation that makes a managed SOC investment actually stick.

Detection and response are only part of the equation. Without a clear governance framework, a documented risk posture, and compliance controls that map to your regulatory obligations, even the best SOC is operating without a blueprint.

Arpatech mitigates that gap, helping mid-sized organizations align their security operations with business risk, satisfy auditors and insurers, and make confident, board-ready decisions about where to invest next.

Make sure someone’s watching. And make sure there’s a program built to last.

Not always.

Many people assume that keeping a SOC in-house makes compliance easier because everything stays under your direct control. In reality, compliance is about process, visibility, documentation, and response, not just location.

A well-run outsourced SOC can meet the same compliance requirements, and often does it more consistently because monitoring, logging, and reporting are handled by specialists who do this every day.

How Arpatech helps:

Arpatech helps you map your SOC operations directly to your compliance needs. Whether your SOC is in-house, outsourced, or hybrid, we make sure the monitoring, reporting, and documentation align with standards like SOC 2, ISO 27001, HIPAA, and others.

for more information, visit our trust center.

The biggest risk is loss of context.

An external SOC team may not fully understand your business, your systems, or what “normal” looks like in your environment. This can lead to slower investigations, false alarms, or missed signals if knowledge transfer is weak.

This risk is not about capability. It is about communication and integration.

Arpatech works as a bridge between your internal teams and the MSSP. We document your environment, workflows, and risk areas so the external SOC is never working in the dark. We ensure proper onboarding, playbooks, and continuous knowledge sharing so your outsourced SOC operates with full context.

A hybrid SOC works best when you want control and expertise at the same time.

This model is ideal when:

In this setup, the external SOC handles monitoring and alerts, while your internal team handles decisions and responses.

At Arpatech, we help you design and implement hybrid SOC models. We define who does what, set up the tools, create the response workflows, and make sure your internal team and the external SOC operate as one unit instead of two separate teams.

Ramsha Khan

May 19, 2026

Patch Management Strategy: Balancing Speed, Security, a...

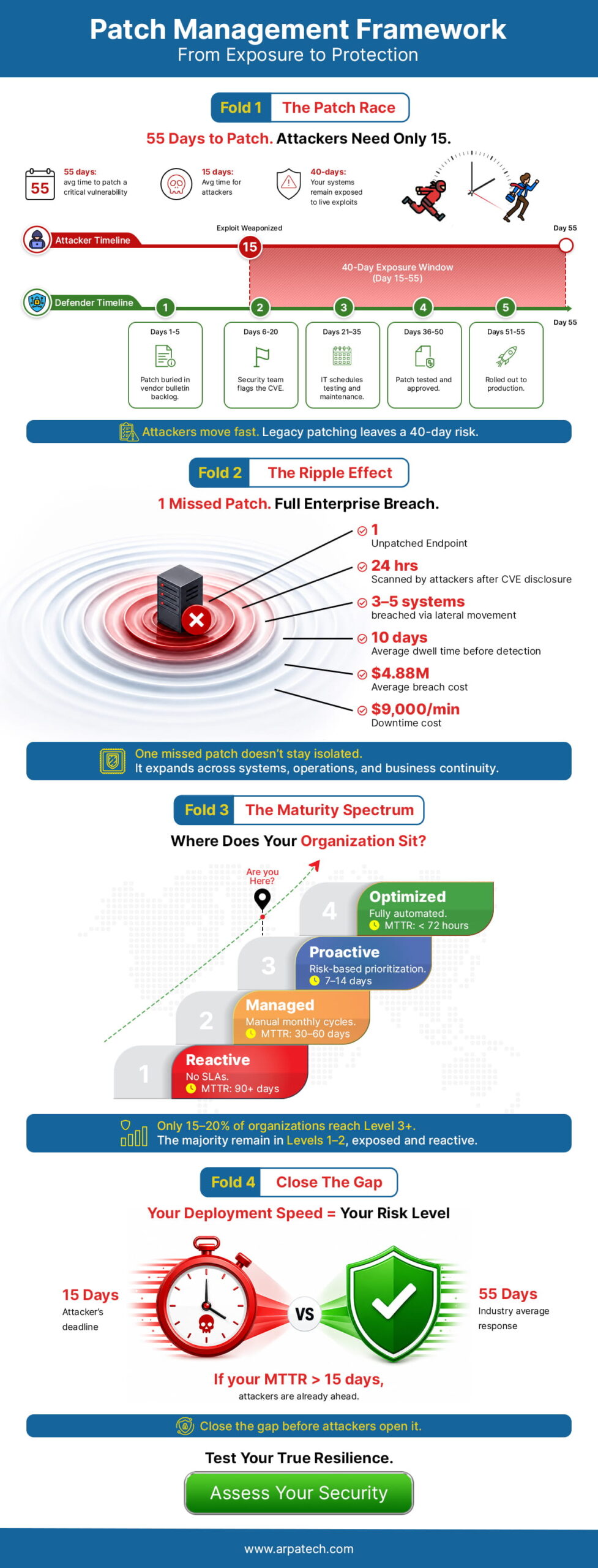

Every few months, a major cyberattack makes national headlines. A hospital gets crippled by ransomware. A retailer exposes millions of customer records. A government contractor suffers a data breach with national security implications. And almost every time, investigators find the same uncomfortable truth buried in the post-mortem: the vulnerability that was exploited had a patch available weeks or even months before the attack. It just was never applied.

That is not a technology problem. It is a strategy problem.

A strong patch management strategy is the difference between an organization that stays ahead of threats and one that is constantly reacting to them. But building that strategy is harder than it sounds. IT teams are stretched thin, business owners resist downtime, legacy systems resist patches entirely, and the volume of vulnerabilities being disclosed every year continues to climb. Getting patching right means finding a way to balance speed, security, and business continuity all at once, and that requires more than just downloading updates when a vendor releases them.

This guide will walk you through everything you need to know, from what is Patch management, understanding why patching fails to building a mature, enterprise-grade approach that actually works.

This blog covers everything you need to know about building a patch management strategy that balances speed, security, and business continuity. Here is what we walk through:

When software companies discover bugs or security flaws in their products, they release fixes called patches. Patch management is the process of identifying, testing, and applying those fixes across your organization’s systems in a consistent, timely way.

Think of it like routine car maintenance. Skip an oil change once and you will probably be fine. Keep ignoring it and you are looking at a much bigger, more expensive problem down the road. Unpatched software works the same way. A single ignored vulnerability can be all an attacker needs to break into your network.

In a business environment, patch management covers everything from operating systems and browsers to network devices and third-party applications. With hundreds of patches released every month across dozens of vendors, having a structured process is not optional. It is the difference between staying ahead of threats and constantly reacting to them

A lot of organizations treat patching like a chore, something IT handles in the background when they get around to it. That mindset is increasingly dangerous. The threat landscape has fundamentally changed. Vulnerability exploitation has become faster, more automated, and more targeted than ever before.

According to the Cybersecurity and Infrastructure Security Agency (CISA), many of the successful ransomware attacks in the US exploit known, patchable vulnerabilities. These are not zero-days or sophisticated nation-state exploits. They are vulnerabilities that already have fixes available. The problem is that organizations are not applying those fixes fast enough, or not applying them at all.

A formal patch management strategy gives IT and security teams a clear, repeatable way to find, test, and install updates across all systems.

It clearly defines who is responsible for what, how quickly patches should be applied, how exceptions are handled, and how progress is tracked. Without this structure, patching becomes random and inconsistent, which increases the chances of missing important updates.

Past security, a proper strategy also helps keep the business running smoothly. Poorly tested patches can break applications, cause downtime, or create new technical issues.

A good approach includes testing updates before release, rolling them out in stages, and having a rollback plan ready. This ensures that fixing one issue does not accidentally create several new ones.

Every IT team must navigate one critical conflict that exists between their two main operational needs. The security measure which provides maximum protection through immediate patching creates operational challenges which users consider highly dangerous. Patches can disrupt current software operations because they lead to unexpected system restarts and they disable custom settings which require extended development time to implement.

This situation establishes a condition which IT specialists refer to as the patch management paradox. Security teams push for speed. IT operations push for stability. Business owners push for uptime. The patching process encounters delays because it requires decision makers to choose between different options that are available at that moment.

The longer patches wait, the more exposure the organization accumulates. But rushing patches into production without testing can cause just as much damage as the vulnerabilities they are meant to fix. A botched patch that takes down a critical ERP system on a Monday morning can cost a company more in lost productivity than the breach it was supposed to prevent.

Resolving this paradox is not about picking a side. It is about building a process sophisticated enough to move quickly on critical vulnerabilities while still protecting operational stability.

That means having different response timelines for different risk levels, having a reliable test environment, and having clear communication channels between security, IT, and the business.

The numbers are hard to ignore. The Ponemon Institute has consistently found that a significant majority of data breaches involve known vulnerabilities that had patches available.

The Verizon Data Breach Investigations Report echoes this year after year. Exploitation of known vulnerabilities is not just common, it is the dominant attack vector for financially motivated threat actors.

The reason is simple economics. Attackers are not trying to be clever. They are trying to be efficient. Writing a custom exploit for an unknown vulnerability takes significant skill and time. Scanning the internet for systems still running a version of software with a known, publicly disclosed vulnerability takes minutes. Tools like Shodan and Censys make it trivially easy for attackers to find exposed systems at scale.

Once a vulnerability is disclosed and a patch is released, the clock starts ticking. Researchers have documented that the time between patch release and widespread exploitation has shrunk dramatically over the past several years. What used to take months now sometimes takes days. In some high-profile cases, weaponized exploits appeared within hours of a vulnerability disclosure.

This means that organizations with slow, reactive patching cycles are operating with a window of exposure that attackers are actively hunting for.

The financial cost of a successful cyberattack in the US has never been higher. IBM’s Cost of a Data Breach Report consistently puts the average cost of a US data breach in the millions, and ransomware incidents routinely run into the tens of millions when you factor in recovery costs, legal fees, regulatory fines, and lost business.

The 2021 Colonial Pipeline ransomware attack, exploited a compromised VPN without multi-factor authentication on a legacy account, this led to fuel shortages across the eastern US and a reported ransom payment of approximately $4.4 million. The 2017 Equifax breach, which exploited an unpatched Apache Struts vulnerability despite a patch being available for months, resulted in a $575 million settlement with the FTC.

These are not irregularities. They are examples of what happens when patching is treated as optional.

Bad patches can also create serious problems. In 2024, a faulty update to the CrowdStrike Falcon sensor caused a global IT outage. Millions of Windows systems stopped working, which disrupted airlines, hospitals, banks, and media companies.

Even though this was a security software update and not an operating system patch, it shows an important lesson: how updates are released matters just as much as the updates themselves.

A strong patch management process helps prevent this kind of failure. It includes proper testing before release, approval steps, and rolling out updates in stages instead of all at once. This reduces the risk of large-scale outages and keeps systems stable.

For US organizations operating in regulated industries, poor patch management is not just a security risk, it is a compliance risk. HIPAA requires healthcare organizations to implement security updates to protect electronic protected health information.

PCI DSS mandates that organizations maintain a process for timely patching of all system components. NIST frameworks, FedRAMP, and SOC 2 all include patching requirements.

Regulators and auditors are increasingly scrutinizing patch compliance. HIPAA penalties can reach $1.9 million per violation category per year. The SEC has also increased its focus on cybersecurity practices, including vulnerability management, for publicly traded companies.

You cannot patch what you do not know exists. Asset inventory is the unglamorous foundation of every effective patch management strategy.

This means maintaining an accurate, continuously updated inventory of every device, operating system, application, and firmware version across the environment, including endpoints, servers, network devices, cloud instances, and operational technology.

Modern automated patch management software can automate much of this, but the process requires ongoing attention. New devices get added, old ones get forgotten, and shadow IT (unauthorized systems and applications that employees spin up without IT approval) creates invisible blind spots that attackers love to find.

Knowing what systems you have is only helpful if you also know what security issues they may have.

Vulnerability scanning tools like Tenable Nessus, Qualys, and Rapid7 help with this. They constantly check your IT environment to find weaknesses in systems and applications.

These tools compare what they find against known security issue databases like the National Vulnerability Database and the CISA Known Exploited Vulnerabilities Catalog, which list publicly known and actively exploited vulnerabilities.

This helps organizations quickly understand which assets are at risk and need urgent patching.

Layering in threat intelligence enriches this further. Not every high-CVSS vulnerability is being actively exploited in the wild, and knowing which ones are actively targeted helps teams allocate limited resources more effectively.

Not all patches are equal, and treating them as if they were is one of the most common and costly mistakes in patch management planning. A critical vulnerability on an internet-facing server that handles payment processing is categorically more urgent than a medium-severity vulnerability on an internal workstation used for scheduling.

Risk-based prioritization considers:

Frameworks like SSVC (Stakeholder-Specific Vulnerability Categorization) or the CISA KEV catalog provide structured ways to make these prioritization decisions systematically rather than intuitively.

Before any patch goes into production, it should be tested in an environment that mirrors production as closely as possible. This catches compatibility issues, application conflicts, and configuration problems before they affect real users and systems.

Testing should include functional testing of affected applications, regression testing to ensure existing functionality is not broken, security validation to confirm the patch actually addresses the vulnerability, and performance testing for patches affecting high-load systems.

Even after testing, patches should be deployed in phases rather than all at once. A phased approach typically starts with a small pilot group (often IT staff or volunteers), expands to a broader test population, and then rolls out to the full environment. This limits the blast radius of any unforeseen issues.

Equally important is verification. Confirming that a patch was successfully installed is not the same as assuming it was. Automated verification scans should confirm patch deployment and flag any endpoints where installation failed or was skipped.

Define who is responsible for identifying vulnerabilities, who approves patches for deployment, who executes deployments, and who verifies success.

In larger organizations, this usually involves a cross-functional patch management team that includes IT operations, security, and representatives from major business units.

Maintenance windows, designated periods when systems can be taken offline for patching, should be established in advance and communicated broadly. Emergency patching procedures for critical zero-day vulnerabilities need separate, expedited approval processes.

Conduct a thorough risk assessment of your entire IT environment. Use automated patch management tools to find every managed and unmanaged device. Pay particular attention to:

Shadow IT is a particular concern. Employees regularly spin up cloud services, install applications, and connect personal devices without IT knowledge. These assets are often the least patched and the most vulnerable.

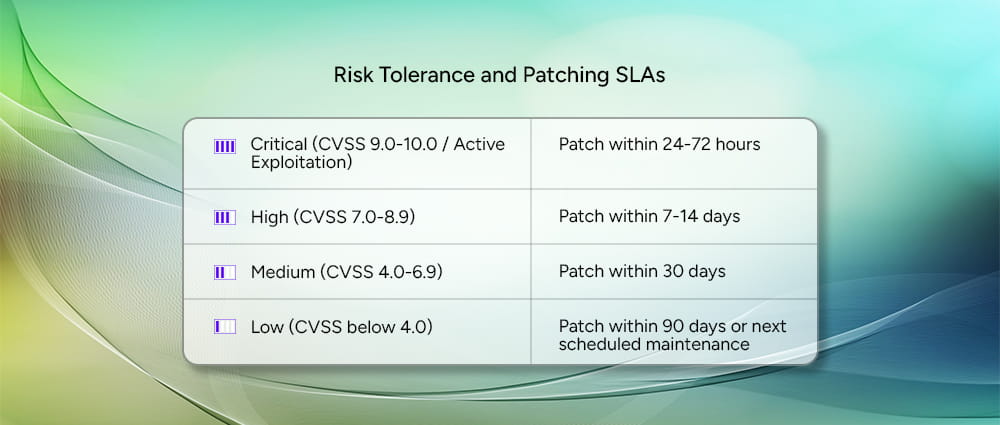

Document clear SLAs for patch deployment based on severity. A common framework looks like this:

Not every vulnerability needs to be treated as an emergency. Critical vulnerabilities, especially those already being actively exploited in the wild, should be patched within 24 to 72 hours. High severity issues give you a slightly longer window of 7 to 14 days, while medium severity vulnerabilities should be resolved within 30 days. Low severity issues are the least urgent and can typically wait until your next scheduled maintenance window, as long as that falls within 90 days.

These SLAs should be formally documented, reviewed annually, and adjusted based on threat intelligence and business risk.

You should create a testing environment which exactly duplicates your actual production systems. The testing environment must include various configurations of essential applications and systems. Organizations need to establish multiple testing environments which serve different business operations and system categories because their operational frameworks are complicated.

Cloud environments make this more accessible than ever. Spinning up a replica environment in AWS or Azure for patch testing is significantly cheaper than it used to be, and it enables faster, more thorough testing cycles.

Every patch deployment should have a documented rollback plan. If a patch causes problems in production, the team needs to be able to revert quickly and cleanly. This requires:

The shift to hybrid and remote work has created a persistent headache for patch management teams. Endpoints that are rarely or never on the corporate network are difficult to inventory, scan, and update through traditional on-premises tools.

The solution involves deploying cloud-based endpoint management platforms (like Microsoft Intune, Jamf, or similar tools) that can reach devices regardless of network location.

VPN usage can be used for scanning, but cloud-native management is increasingly the preferred approach for modern distributed workforces.

Many US organizations, particularly in manufacturing, healthcare, and government, run critical systems on operating systems and applications that vendors no longer support. Windows Server 2008, Windows 7, and older versions of industrial control software continue to run critical infrastructure despite being years past end-of-life.

When patches are simply not available, compensating controls become essential. Network segmentation isolates legacy systems from the rest of the environment.

Web application firewalls and intrusion prevention systems can provide virtual patching. Strict access controls and monitoring add additional layers of protection.

IT teams hear “no” from business owners all the time when it comes to patching. The reasons are usually the same: we can’t afford the downtime, or the last update broke something important. Those concerns are fair, and dismissing them only makes the relationship worse.

The fix is to stop speaking in technical terms and start speaking in business language. A business owner does not know what a CVSS score is. What they do understand is money and time. Tell them that skipping this patch leaves their ERP system exposed to a ransomware attack that could shut operations down for a week, and suddenly a two-hour maintenance window sounds a lot more reasonable.

It also helps to have a formal exception process. Give business owners a legitimate way to request a delay, document the risk they are accepting, and put temporary safeguards in place in the meantime. People push back less when they feel heard and have options rather than just a deadline.

Security teams use tools that find weaknesses in systems, while IT teams use separate tools to install updates and manage devices. The problem is that these tools often don’t connect with each other. This means vulnerability information stays in one system, while the actual fixing work happens in another.

When these systems are connected using integrations, APIs, or automation platforms, the process becomes much smoother. For example, when a serious vulnerability is detected, the system can automatically create a task in the IT service system, assign it to the right team, and track it until the issue is fully fixed and confirmed.

Here are some advanced strategies that IT professionals should know about patch management that can help them get rid of vulnerabilities faster and more effectively.

Virtual patching uses network-level controls like intrusion prevention systems and web application firewalls to block exploit attempts against known vulnerabilities without actually modifying the vulnerable system.

It is not a permanent solution, but it is an important bridge for assets that cannot be immediately patched.

Network segmentation limits the blast radius if a vulnerable system is compromised. By placing legacy and unpatchable systems in isolated network segments with strict access controls and traffic monitoring, organizations can contain the damage from a successful exploit.

For organizations with active software development, patch management cannot be separate from the development process. Integrating vulnerability scanning into CI/CD pipelines ensures that base images, container dependencies, and third-party libraries are scanned for vulnerabilities before code is deployed.

This shifts patching left, catching issues earlier in the development process when they are cheaper and easier to fix. Tools like Snyk, Dependabot, and Prisma Cloud integrate directly into development workflows to automate this process.

Traditional patching, where you find a vulnerability and push a fix to a running system, does not really work in modern cloud environments.

With containers, you do not patch the running container. You update the base image it was built from and rebuild it. That means keeping those base images current and regularly scanning your container library for vulnerabilities is how patching works in this world.

Serverless is a bit different. The cloud provider (AWS, Azure, Google Cloud) handles patching the underlying infrastructure for you. But the code your developers wrote, and the third-party libraries it depends on, are still your responsibility. Automated patch management software that scan those dependencies and flag outdated or vulnerable packages are what keep serverless environments secure.

Managing patches manually across a large organization is not realistic. When you have thousands of devices, hundreds of applications, and a constantly changing environment, there is simply no way for a human team to keep up without help.