If you’ve ever filed an insurance claim, you know the drill: forms, back-and-forth emails, waiting for verification, then waiting some more for payment. In 2025, that experience is getting a serious upgrade. The catalyst? blockchain smart contracts insurance solutions that bring automated claims processing, trust, and transparency to every step.

Think of a smart contract as a tiny program that lives on a blockchain. It holds the rules of your policy (what’s covered, how much, under what conditions) and it can automatically run those rules when certain events happen. Instead of humans pushing paper, software enforces the policy. The result is blockchain claims automation that shortens timelines, reduces disputes, and helps carriers scale efficiently.

Let’s unpack how it actually works, and where it’s already making a difference.

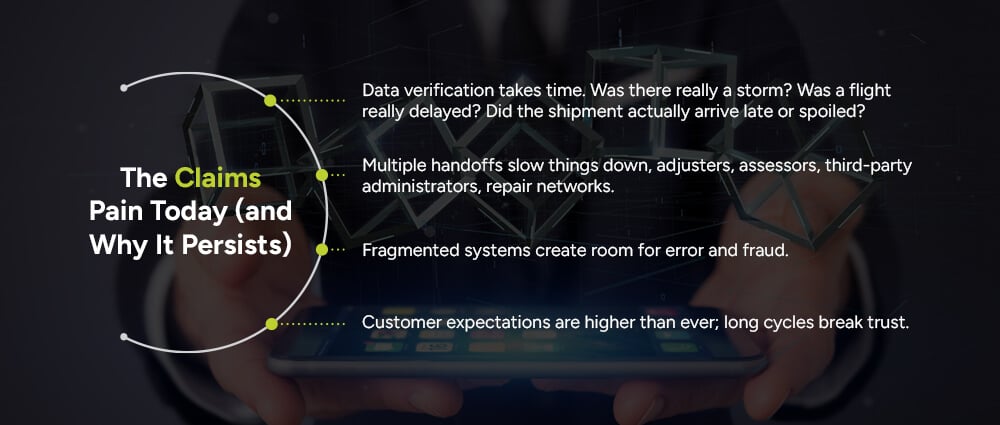

Modern insurers have big investments in digital claims management, but several challenges persist:

To better understand the challenge, consider one current benchmark: J.D. Power reported that U.S. auto repair cycle times during 2024 averaged 18.9 days later in the fielding period, down from 23.9 days earlier, but still weeks of waiting for many customers.

That context matters: any insurance technology innovation that can reduce verification time, automate payouts, and remove redundant steps represents a significant improvement.

A smart contract is basically the policy logic turned into code and deployed on a blockchain. Here’s how that changes the game for digital insurance transformation:

The rules you see in your policy PDF, deductibles, coverage limits, and exclusions, become program logic. If X happens and the evidence meets condition Y, the contract triggers outcome Z. This is insurance process optimization at its core.

Smart contracts don’t guess. They wait for cryptographic proof or reliable data from oracles (secure data bridges) to confirm an event. This is the backbone of blockchain claims verification.

Once the trigger is verified, the contract can initiate automated insurance settlements: releasing a payment, notifying a bank, sending instructions to a repair partner, or updating the claim’s status. Manual intervention occurs only for exceptions.

All decision steps are recorded, reducing disputes and simplifying compliance. Auditors can easily verify what happened, when it occurred, and why.

The result: actual blockchain insurance efficiency. There is less back-and-forth, fewer manual checks, quicker decisions, and consistent outcomes.

Smart contracts shine brightest in smart contract use cases, such as insurance, where the loss event is objective and data-driven. That’s why parametric products, policies that pay when a measurable trigger occurs, have become the poster child for blockchain claims automation.

These are high-fit use cases because the truth lives in data, exactly what smart contracts consume.

Here’s what the process typically looks like when implementing a smart contract for insurance claims:

A data oracle provides secure, tamper-resistant feeds like weather readings, IoT sensor data, shipping milestones, flight schedules, mortality records, or verified documents. Smart contracts monitor these inputs and automatically act when predefined thresholds are met.

The smart contract compares incoming data with the policy logic: “Was rainfall under 10 mm for 15 consecutive days?” “Was the shipment temperature above 8°C for more than 30 minutes?” This is the blockchain smart contracts insurance brain at work.

When conditions are met, the contract executes actions such as initiating payment, notifying stakeholders, closing the claim, or triggering further checks. With automated claims processing, settlement can be almost in real time, with support for simple cases.

Case studies highlight the importance of secure oracles that supply smart contracts with tamper-resistant data, especially in parametric models where automation is a key feature.

The benefits for policyholders are straightforward: faster claims and more certainty. With smart contract insurance, customers experience:

For insurers, optimizing the claims process means lower handling costs, smoother customer experiences, and the ability to free adjusters to focus on complex claims.

One forward-looking benchmark: McKinsey predicts that by 2030, more than half of current claims activities could be replaced by automation, a signpost for the industry’s direction and a strong rationale for investing in claims automation now.

You’ll see the earliest and cleanest wins in lines of business with objective data triggers:

As confidence increases, insurers are incorporating smart contracts into traditional indemnity claims. They use blockchain to verify documents, log adjuster decisions, manage vendors, and automate partial payments during repairs. This represents a real-world example of hybrid digital claims management in action.

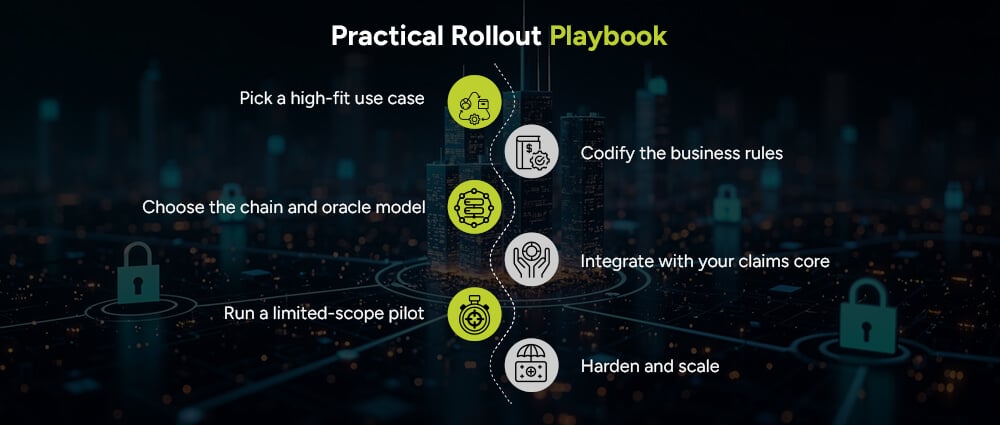

A practical smart contract implementation insurance blueprint usually looks like this:

Insurers don’t need to move their entire tech stack to blockchain.Instead, many are simply integrating a smart-contract layer that connects to existing systems through APIs, providing an incremental approach to digital insurance transformation.

Smart contracts are code, so treat them like critical software:

Done right, GRC becomes a blockchain insurance efficiency driver, not a blocker.

Even with clear benefits, executives want numbers. Teams can justify their investment by highlighting:

Remember our baseline: multi-week auto claim cycles are common today, and projections indicate that a significant portion of claims activity will trend toward automation by 2030. These two facts alone provide a compelling case to pilot blockchain claims automation now.

A successful smart contract implementation relies on an iterative, step-by-step approach.

Focus on areas such as travel delays, weather-based policies, objective triggers, and reliable data.

Convert policy text into specific rules with conditions like thresholds, time frames, and coverage limits.

Permissioned vs. public with privacy layers; single or multiple data oracles; fallback logic for missing data.

Connect read/write APIs to your FNOL intake and other systems, using lightweight middleware for event orchestration.

Conduct a Pilot

Implement a pilot with real customers and payouts in a limited area, measuring speed, service, dispute rates, and customer satisfaction.

Incorporate additional data feeds, expand geographical coverage, and introduce hybrid models that automate certain aspects of indemnity claims, such as document checks and payment triggers at specific milestones.

By following this approach, you can transform“innovation theater” into tangible improvements in insurance process optimization.

By 2025, smart contracts will transition from concept to core capability. When you strip away the buzzwords, you’re left with something both simple and powerful: policy rules that enforce themselves when trusted data says it’s time. That’s the essence of blockchain smart contracts insurance, and it’s why customers and carriers are feeling the difference.

Use cases that leverage objective, third-party data are already showing significant results, while more complex claims are benefiting from automated checkpoints that reduce processes and accelerate settlements. With only a modest effort required to integrate, insurers can unlock faster, fairer, and more transparent claims, exactly what policyholders have wanted all along.

At Arpatech, we help insurers and enterprises bring these innovations to life. From building secure smart contract frameworks to integrating blockchain with your existing claims systems, our team ensures a smooth transition toward digital insurance transformation. Whether you’re piloting parametric covers or modernizing traditional claims workflows, the consultants at Arpatech provide the expertise, technology, and support to make automated claims processing a practical reality for your business.

They automate the busywork. Instead of people collecting and checking evidence step by step, the contract listens for trusted event data (like verified flight delays, weather indices, or IoT sensor readings). When conditions match the policy rules, it triggers actions automatically, like approving the claim or initiating payment. This removes handoffs and compresses cycle time, a major goal of digital claims management and insurance technology innovation.

Common triggers in smart contract use cases insurance include:

Start where proof is objective, and coverage is binary: parametric travel, weather-indexed agri, and cargo/IoT-based policies. From there, layer automation into parts of traditional claims: document checks, milestone-based partial payouts, and vendor orchestration. This staged approach delivers early value while you build toward broader blockchain insurance efficiency.

Before we begin, please solve this quick math check to confirm you're human, and you'll be all set to start chatting with our AI assistant.

Stay connected with us to receive the latest information, updates, and insights from our world of innovation.

By entering your email address you will receive promotional updates.

© 2026 ARPATECH (ADVANCED RESEARCH PROJECTS & TECHNOLOGY)